Automated Journal Entries: A Complete Guide for Accurate Accounting

Have you ever finished a long day of manually entering numbers, only to realize you still have to hunt down a tiny mistake that threw everything off? Or felt that familiar knot in your stomach as month-end crept closer, knowing you'd be glued to spreadsheets for hours? If that sounds familiar, you're far from alone. Many business owners and finance teams quietly dread the routine of recording transactions the old-fashioned way.

Automated journal entries change that story entirely. They quietly remove most of the repetitive, error-prone work, hand back large chunks of time, and let you look at your financials with genuine confidence instead of second-guessing. It's not about flashy tech for the sake of it, it's about making your Bookkeeping feel lighter so you can focus on what actually grows your business.

Here's how it really plays out in day-to-day life: your accounting software sits in the background like a dependable teammate. It automatically pulls fresh transaction details from connected places, bank statements, incoming invoices, payroll runs, expense submissions, card swipes, and more. Then it creates balanced journal entries without you typing a single line. No more manual debits and credits, no copy-paste slip-ups, no wondering if something got missed.

For small businesses, startups, and companies scaling quickly, this often becomes the moment everything starts to feel manageable again. Repetitive tasks fade away, costly human errors drop sharply, and your financial reports become clear, trustworthy documents that make sense to you, your accountant, your bank, or investors.

In the fast-moving world of digital finance today, sticking with purely manual processes adds unnecessary pressure and slows down growth. Modern accounting automation has shifted from nice to have to a real advantage, one that delivers smoother day-to-day flows, easier scaling, stronger oversight, and more space to focus on strategy and customers.

At Accounts Junction, we see this shift happen for clients all the time. Businesses that once felt buried in paperwork suddenly breathe easier and move faster.

This guide is written in plain, straightforward language to help you understand the full picture. We'll cover exactly what automated journal entries are, how the process works from start to finish, the benefits that matter most to real business owners, practical examples you’ll recognize from your own operations, sensible tips to implement them well, and the ways they help you manage finances with far less stress and more clarity.

What Are Automated Journal Entries?

Simply put, automated journal entries are financial records your software creates on its own, the instant a transaction or event happens.

You no longer have to open a spreadsheet or accounting screen and enter every detail manually. Instead, the system follows clear rules you set once—rules that tell it exactly which accounts to debit and credit for different types of transactions.

The payoff is easy to see:

- Entries remain perfectly consistent month after month no random variations depending on who entered them.

- Accuracy jumps dramatically because the chance of typos or miscalculations shrinks to almost nothing.

- Every day, bookkeeping moves much faster, so routine work no longer eats up entire afternoons.

It genuinely feels like having a quiet, ultra-reliable assistant who handles the boring parts flawlessly every single time, letting you trust the numbers without constant double-checking.

Why More Businesses Are Making the Switch

Manual journal entries take time, mental energy, and focus. Even careful people occasionally make small slips, wrong accounts, missed decimals, forgotten adjustments, and those little things can create bigger headaches later, especially when it’s time for taxes, audits, or sharing reports.

That’s why companies of all sizes are turning to automated journal entries. The main reasons usually boil down to wanting to:

- Stop repeating the same data entry over and over.

- Build far greater confidence in bookkeeping accuracy.

- Finish the month-end close in a fraction of the usual time, with much less stress.

- Keep every record uniform and professional-looking.

- Make audits, compliance reviews, and tax reporting feel routine instead of scary.

When your business starts handling more volume, more sales, more vendors, and more employees, manual methods quickly become a bottleneck. Automation clears that roadblock, letting you grow without adding endless hours of extra work.

How the Process Actually Works

The magic of automated journal entries comes from three connected pieces that work together smoothly.

First comes pre-set rules. Your accountant defines the logic once: When this type of sale happens, debit this account and credit that one. The software then applies those instructions instantly for every matching transaction.

Second, connected data sources bring everything together. Bank feeds update automatically, payment gateways send transaction info, invoicing tools push out invoices, payroll systems run salaries and deductions, expense apps capture receipts—the data flows straight in, triggering journal entries the moment it arrives.

Third, AI in accounting adds intelligence. Modern tools use artificial intelligence to classify transactions smarter, spot anything unusual, and suggest improvements over time, so accuracy keeps getting better without extra effort.

Set it up once properly, and the system runs reliably in the background, especially when you’re using solid cloud accounting software that handles integrations well.

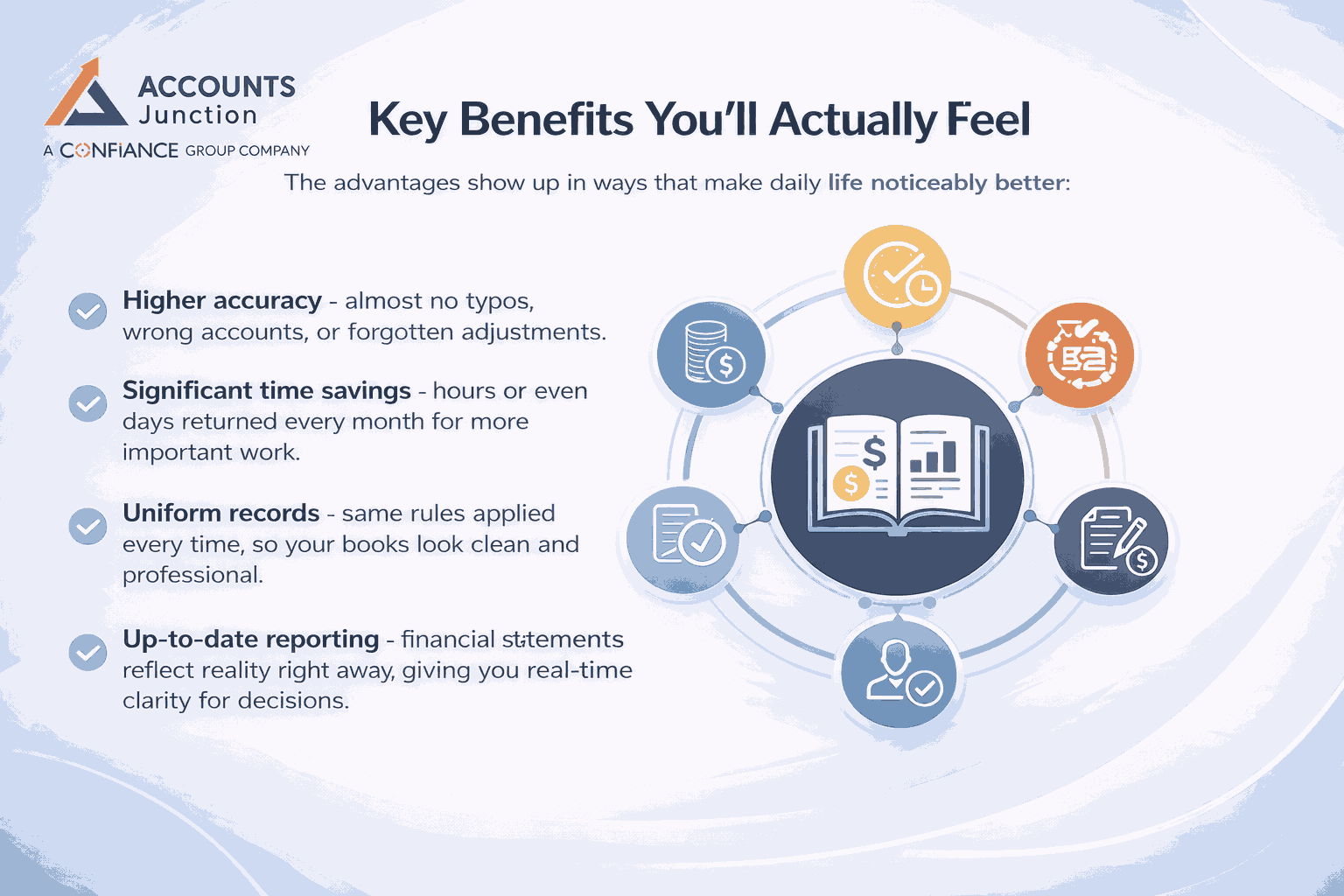

Key Benefits You’ll Actually Feel

The advantages show up in ways that make daily life noticeably better:

- Higher accuracy - almost no typos, wrong accounts, or forgotten adjustments.

- Significant time savings- hours or even days returned every month for more important work.

- Uniform records - same rules applied every time, so your books look clean and professional.

- Up-to-date reporting - financial statements reflect reality right away, giving you real-time clarity for decisions.

-

Together, these create less daily stress, sharper insights, and a business that feels more in control.

Everyday Examples from Real Operations

See how this looks in common situations:

- Customer sales - send an invoice or receive payment, and the revenue entry appears automatically with taxes and discounts handled.

- Business expenses - a card purchase or employee expense claim is submitted, and the entry is created instantly in the right category.

- Payroll runs - salaries, taxes, benefits post correctly without anyone typing them in manually.

- Fixed assets - monthly depreciation is calculated and recorded on schedule, consistently every period.

- These ordinary activities stop being time-consuming chores and become background processes that just work.

Automated vs Manual - A Straightforward Comparison

Speed and reliability - automation is dramatically faster and commits far fewer mistakes.

Growth readiness - manual entry buckles as volume rises; automated systems scale smoothly.

Long-term cost - yes, good tools have an upfront cost, but reduced labor, fewer corrections, and quicker closes usually pay for themselves quickly.

Who Gets the Biggest Wins?

Automated journal entries deliver the most value to:

- Small and medium businesses with steady recurring activity

- Startups gearing up for fast expansion

- Teams are already comfortable with cloud accounting

- Owners who value real-time financial insights

- Even so, human oversight still matters for unusual or complex cases. Automation supports people, it doesn’t replace them.

Mistakes to Steer Clear Of

Watch out for these common slips:

- Skipping regular reviews of automated postings

- Using outdated or mismatched account rules

- Ignoring system alerts and exception reports

- Forcing automation onto highly irregular transactions

- A bit of routine attention keeps everything accurate and audit-ready.

Practical Tips for Getting the Best Results

Start strong with these steps:

- Build clear, well-documented rules at the beginning

- Schedule short monthly reviews of recent entries

- Treat automation as a powerful helper for your accounting team, not a full replacement

- Begin small, automate one area like expenses first, then expand once you’re comfortable.

Better Financial Visibility & Control

You end up with:

- Instant awareness of transactions as they happen

- Clearer cash flow tracking

- Quicker month-end close

- Clean audit trails that make reviews straightforward

Staying Compliant Without the Stress

Automated journal entries naturally produce consistent documentation, a traceable history, and reliable data for tax reporting and compliance, making it feel manageable instead of overwhelming.

Looking Ahead

The future holds even better tools: smarter AI in accounting classification, predictive insights, and tighter integrations across business apps. The core idea of automatic journal creation is here to stay and will keep evolving.

Final Thoughts

When implemented thoughtfully, automated journal entries simplify daily routines, reduce errors, and give you a much clearer view of your financial health. The biggest reward is shifting your focus from paperwork to real growth opportunities.

At Accounts Junction, we know the strongest results come from pairing smart automation with solid accounting basics and experienced guidance. If you’re ready to make your books easier to handle and more dependable, we’d love to show you how automated journal entries can fit your business perfectly.

FAQs

1. What are automated journal entries?

They’re journal entries your accounting software creates automatically whenever a transaction happens, no manual typing needed. The software uses simple rules you set to post the right debits and credits.

2. How do they save time?

They grab info straight from your bank, invoices, payroll, whatever’s connected—and post it automatically. That means you skip typing everything by hand, which can easily shave hours (or even days) off your monthly routine.

3. Are automated journal entries accurate?

Yes, way more accurate than manual entry. They cut out typos and mistakes, especially when rules are set right, and you do a quick monthly review.

4. Are they good for small businesses?

Totally. For small businesses and startups, it’s a lifesaver—no extra hires needed, fewer costly slip-ups, and financial reports that actually make sense at a glance.

5. Do they replace accountants?

No. They handle the routine work so accountants can focus on reviewing, planning, taxes, and giving you smart advice.